Euro area countries have relied extensively on fiscal policy to counter the harmful impact of the coronavirus (COVID-19) pandemic on their economies. They have implemented a broad range of measures, some with an immediate budgetary impact and others, such as liquidity measures, which, in principle, are not expected to cause an immediate deterioration in the fiscal outlook. Since all euro area countries were hit by the economic shock largely through the same channels, their fiscal responses in the early stages of the crisis were similar in terms of the instruments used. Fiscal emergency packages were mostly aimed at limiting the economic fallout from containment measures through direct measures to protect firms and workers in the affected industries. Simultaneously, extensive liquidity support measures in the form of tax deferrals and State guarantees were announced to help firms particularly impacted by the containment policies to avoid liquidity shortages. In order to support the recovery, fiscal policy needs to provide targeted and mostly temporary stimulus, tailored to the specific characteristics of the crisis and countries’ fiscal positions. Government investments, complemented by the Next Generation EU package, and accompanied by appropriate structural policies, should play a major role in this respect.

1 Introduction

This article discusses the initial fiscal policy responses of euro area countries to the COVID-19 crisis and the implications for further policy measures. It examines the specific fiscal policy measures taken in the course of 2020 and elaborates on the experiences of euro area countries during the pandemic. The article finds that successful recovery strategies from previous crisis episodes cannot be replicated without being adapted to the current crisis’ circumstances. Looking forward, it discusses the implications for the fiscal stance and considers the main policy questions such as the design and timing of fiscal measures.

Fiscal policy is the most suitable instrument for addressing the detrimental impact of the pandemic on the economy, as it is well equipped to differentiate and channel economic support to where it is most needed. First and foremost, by providing adequate public health care, fiscal policies can help in dealing with the immediate health consequences of the pandemic, which is also a prerequisite for countering the economic effects of the health crisis. Moreover, fiscal policy can alleviate the negative impact of the crisis by bolstering aggregate demand and providing well targeted support to vulnerable households and firms. Overall, fiscal policies have supported the euro area economy in two ways: through the functioning of automatic stabilisers and discretionary actions. In general, automatic stabilisers are sizeable in euro area countries and are effective in cushioning economic shocks. However, the severity and particularities of the COVID-19 crisis, with both demand and supply significantly affected, in particular during the lockdown phases, required the use of significant discretionary fiscal support measures.

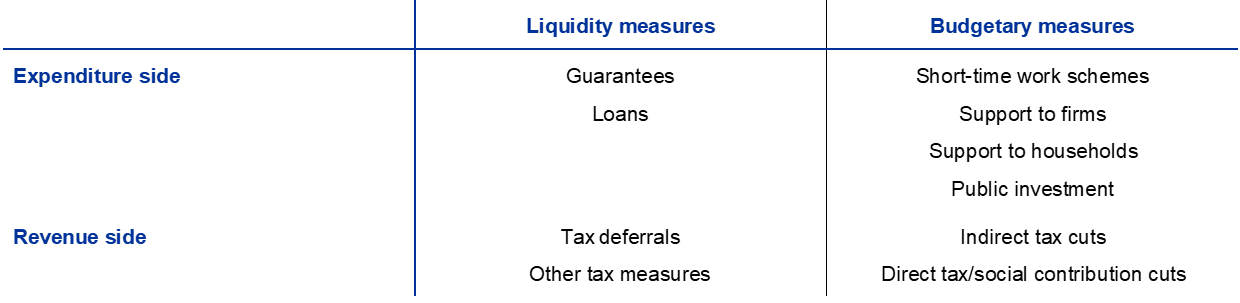

A wide range of discretionary fiscal instruments was implemented or announced in 2020. The fiscal policy reactions were unparalleled in size and scope, as the COVID-19 pandemic and its economic implications posed specific challenges, leading to multi-measure fiscal policy responses. The measures taken by countries can be roughly categorised into two categories: (i) budgetary measures, which typically have an immediate effect on the budget balance, and (ii) liquidity measures, which typically do not immediately affect the budget balance in the year in which they are implemented, but imply contingent liabilities that may affect the fiscal positions. These two types of fiscal measure affect both the expenditure and the revenue side of government budgets (see Table 1).

Table 1

Categories of fiscal instrument

The fiscal interventions took account of the particular challenges posed by the pandemic. First, in the initial phase of the crisis, emergency packages consisting of both liquidity support and budgetary measures were announced to cope with the first phase of broad lockdowns in March 2020, when all euro area countries introduced strict restrictions on businesses and movement of people. Those measures were aimed at supporting the firms and households particularly affected by the health crisis. These emergency measures were renewed, albeit to a lesser extent, towards the end of 2020, when Member States had to introduce partial or “lighter” lockdowns to address the second wave of the pandemic. Second, additional measures were gradually introduced during the interim phase that followed the phasing out of most lockdown measures in mid-2020 in order to support the recovery. In this phase, most businesses reopened, but some sectors were still impaired by ongoing health measures and local and targeted shutdowns, as well as changed consumer behaviour and preferences. Third, further recovery measures are envisaged which are aimed at the more medium to long-term challenges that may arise once the health-related restrictions come to an end.

This article consists of seven sections. Section 2 presents the overall fiscal policy response during the initial phases of the crisis. The subsequent sections review in detail the various measures introduced. Budgetary and liquidity measures on the expenditure side are discussed in Sections 3 and 4 respectively. Sections 5 and 6 give an overview of budgetary and liquidity measures on the revenue side. Section 7 elaborates on the challenges associated with the assessment of the fiscal stance using standard measures, and Section 8 concludes.

Authors:

- Stephan Haroutunian

- Steffen Osterloh

- Kamila Sławińska

Compliments of the European Central Bank.