Fear that the spread of the Delta mutation of the covid would disrupt the global economy spurred the unwinding of risk-on positions. Interest rates fell, and the traditional funding currencies: the US dollar, Swiss franc, and Japanese yen, strengthened most in July. While major US indices set new record highs, as did Europe’s Dow Jones Stoxx 600, the MSCI Emerging Markets Equity Index fell 7%.

The preliminary July PMI reports were below expectations in the US, UK, and France. Japan’s composite PMI has been contracting since February 2020. There has been some re-introduction of social restrictions in parts of Europe. The UK’s “Freedom Day” (July 19), when mask requirements and social restrictions were supposed to be dropped, turned into a caricature as the Prime Minister and Health Minister were in self-quarantine due to exposure, and the number of cases reached the highest level in 5-6 months.

Given the large number of people in the world that remain unvaccinated, the challenge is that the virus will continue to mutate. Moreover, even in high-income countries, where vaccines are readily available, and stockpiles exist, a substantial minority refuse to be inoculated. This is encouraging the use of more forceful incentives that deny the non-vaccinated access to some social activity in parts of the US and Europe. In the US, the vaccines have been approved for emergency use only, and broader approval by the FDA could help ease some of the vaccine hesitancy. Yet, rushing the process would be self-defeating. An announcement still seems to be at least a couple of months away.

In some countries, the surge in the virus even where not leading to hospitalizations and fatalities, maybe tempering activity and postponing more “normalization” like returning to offices. The increase in the contagion has also prompted several companies to postpone plans to have employees return to offices. In other countries, like Australia, the virus and social restrictions are having a more dramatic economic impact. Its preliminary July PMI crashed to 45.2 from 56.7, the lowest since last May. Although many countries in East Asia seemed to do well with the initial wave, they have been hard hit by the new mutations. For some, the recovery already had appeared to be in advanced stages.

Floods in China, India, Germany, and Belgium add to the economic angst. A freeze in Brazil sent coffee prices percolating higher. Wildfires in Canada stopped the downside correction in lumber prices. While rebuilding is stimulative, in the first instance, the natural disasters could be inflationary as transportation and distribution networks are impacted.

The market reacted by pushing down nominal and real interest rates. In late July, the US 10-year inflation-protected note yield (real rate) fell to a record low near minus 1.13% Ten-year benchmark yields in the US, Europe, Australia, and China were at 4-5 month lows. Expectations for rate hikes by high-income countries eased, and Beijing surprised investors by cutting reserve requirements by 50 bp (freed up ~$150 bln of liquidity).

Still, other central banks, like Russia who hiked rates by 100 bp in late July, are pushing forward. In Latin America, Brazil, Mexico, and Chile are likely candidates for rate hikes in August. The market anticipates additional rates hikes from the Czech Republic and Hungary. On the other hand, Turkey’s central bank meets under much political pressure to cut rates. Inflation is not cooperating, and it reached 17.5% in June, a new two-year high. Yet, the Turkish lira downside momentum eased, and this alone, in the face of a stronger dollar, meant it was the best performing emerging market currency last month, up about 3.0%. Its 12% loss year-to-date still makes it the second-worst performing emerging market currency so far this year, behind the Argentine peso’s nearly 13% decline.

The Federal Reserve does not meet in August, but the Jackson Hole symposium (August 26-28) may offer a window into official thinking about the pace and composition of its bond purchases. Under that scenario, a more formal statement would be provided at the end of the September FOMC meeting (September 21-22). Chair Powell has pledged to give ample notice about its plans to taper. This means that the initial timing of the beginning of the tapering may be vague by necessity. Many expect the Fed to begin reducing its bond purchases either later this year or early next year.

The debt ceiling debate may add another wrinkle. The debt ceiling waiver expired at the end of July. There are several different ways that Treasury can buy time. There are many moving parts, and it is hard to know exactly when Secretary Yellen would run out of maneuvers, but she probably has around two months. In the past, the uncertainty was reflected in some T-bill sales. Recall it was the debate over the debt ceiling (the government has already made the commitments or spent the funds and now has to pay for them) that prompted S&P to remove its AAA rating for the US in 2011.

Meanwhile, Beijing is waging an internal battle to retain control in the technology and payments space. It has also stepped up its antitrust actions and moved to make it more difficult for internet companies to have IPOs abroad. At the same time, the US threatens to de-list foreign (Chinese) companies if they refuse to allow US regulators to review their financial audits. This is more than quitting before getting fired, though at the end of July the US announced that concerns over risk disclosures have prompt it to freeze applications for Chinese IPOs and the sale of other securities. Its efforts to turn the private schools into non-for-profits are driven by Beijing’s domestic considerations, but foreign investors–hedge funds, a couple US state pension funds, and provincial pensions in Canada appear to have been collateral damage. Even the Monetary Authority of Singapore had exposure.

The jump in Chinese yields and the drop in equities that pushed the CSI 300 (an index of large companies listed on the Shanghai and Shenzhen exchanges) 21% below the February peak prompted some remedial measures by officials. They succeeded in steadying the bonds and stock markets, and the yuan recovered from three-month lows as July wound down. However, both the disruption and the salve, the selling of industrial metals, coal, and oil from its strategic reserves, demonstrate the activist state that gives foreign investors reservations about increasing allocations to China. To draw foreign capital, officials may be tempted to engineer or facility a strong recovery in shares and the yuan.

Beijing is also meeting resistance from abroad. Its aggressiveness in the region, including the aerial harassment of Taiwan and rejection of the Arbitration Tribunal at the Hague regarding the United Nations Convention on the Law of the Sea (that pushed back against Chinese claims in the South and East China Seas). Over the past few weeks, the situation has escalated. The UK announced it will station two naval vessels in the area. Japan has promised to defend Taiwan should it be attacked by China. The US has not been that unequivocal. The EU has been emboldened. Latvia became the first EU member to open a representative office of “Taiwan” instead of Taipei.

Many wargame scenarios are premised on China attacking Taiwan, but this does not seem to be the most likely scenario. Top US military officials have testified before Congress that Beijing wants to have the ability to invade and hold Taiwan within six years based on comments from President Xi to the People’s Liberation Army. Yet, if China senses that the status of Taiwan is truly changing, it could move against the Pratas Island, which is off the east coast of China and the south tip of Taiwan. It is closer to Hong Kong than Taiwan. It is an uninhabited atoll with a garrison. Taking this island would send a signal about its determination, with the costs and risks of invading Taiwan. It is true to the ancient Chinese idiom about killing a chicken scares the monkeys.

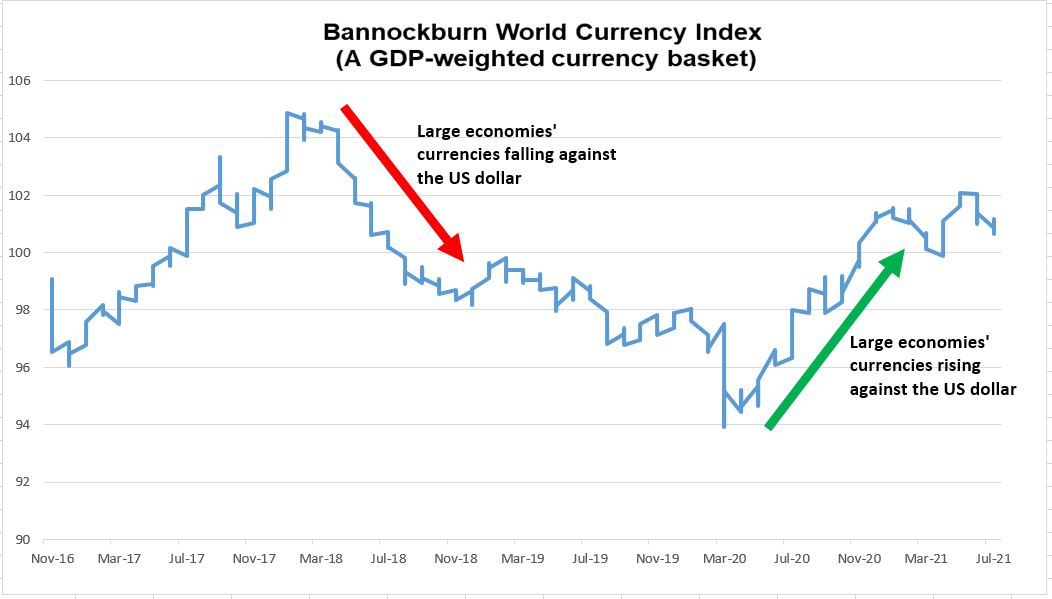

Bannockburn’s World Currency Index, a GDP-weighted basket of the top dozen economies, rose fractionally after falling 1% in June. The two largest components after the dollar are the euro and yuan. The former slipped by was virtually flat near $1.1860 and the latter softened by less than 0.1 %. The yen, with about a 7.3% weighting in the basket, was the strongest, gaining about 1.25% against the US dollar. Sterling was almost eked a 0.5% gain. The Indian rupee slipped 0.1%, while Brazil’s real was the weakest currency in the index, falling by about 4.6% in July.

Dollar: The greenback’s two-month uptrend stalled in the second half of July, sending the momentum traders and late longs to the sidelines. The dollar’s pullback had already begun before the FOMC meeting at which the Fed lent support to priors about a tapering announcement in the coming months. The next opportunity is in late August. The weaker dollar tone that we expect to carry into August could create the conditions that make a short-covering bounce ahead of the Jackson Hole symposium more likely. Some assistance, like the moratorium on evictions, ended on July 31, and others, like the federal emergency unemployment compensation (where states continue to participate), are finishing in early September. Meanwhile, the Biden administration appears to see some of its infrastructure initiative approved in a bipartisan way and the other part through a reconciliation mechanism that it can do if there is unanimous support from the Senate Democrats. Inflation remains elevated, and Treasury Secretary Yellen and Federal Reserve Chair Powell warned it may remain so for several more months but still expect the pressure to subside. The price components of the PMI have eased in the last two reports. There appears to have been some normalization in used car inventories that also reduce the pressure emanating from the one item alone that has accounted for about a third of the monthly increase of late.

Euro: The leg lower that began in late May from around $1.2265 extended more than we had expected and did not find support until it approached $1.1750 in the second half of July. A trough appears to have been forged, and the euro finished near the month’s highs. Technical indicators favor a further recovery in August. Overcoming the band of resistance in the $1.1950-$1.2000 shift the focus back to the highs. The low for longer stance by the ECB may be bullish for European stocks and bonds. The Dow Jones Stoxx 600 reached new record highs in late July. Bond prices are near their highest levels since February-March. The IMF raised its 2021 growth forecast for the euro area to 4.6%from the 4.3% projection in April and 4.3% next year from 3.8%. The economy seemed to be accelerating in Q3, but the contagion and new social restrictions may slow the momentum. Inflation is elevated about the ECB’s new symmetrical 2% inflation target, but it pre-emptively indicated it would resist the temptation of prematurely tightening financial conditions. The debate at the ECB does not seem about near-term policy as much as the commitment and thresholds for future action.

(July 30, indicative closing prices, previous in parentheses)

Spot: $1.1870 ($1.1860)

Median Bloomberg One-month Forecast $1.1885 ($1.1950)

One-month forward $1.1880 ($1.1865) One-month implied vol 5.3% (5.6%)

Japanese Yen: The correlation of the exchange rate with the 10-year US yield is at its highest level in a little more than a year (~0.65, 60-day rolling correlation at the level of differences). The correlation of equities (S&P 500) and the exchange rate is in the unusual situation of being inverse since early this year. In early July, it was the most inverse (~-0.34) in nine years but recovered to finish the month almost flat. The yen rose by about 1.4% in July, offsetting the June decline of the same magnitude. Its 5.7% loss year-to-date is the most among the major currencies and the second weakest in the region after the Thai Baht’s nearly 9% loss. The JPY110.60-JPY110.70 represents a near-term cap. The JPY109.00 area should offer support, and a break would target JPY108.25-JPY108.50. The extension of social restrictions in the face of rising covid cases is delaying the anticipated second-half recovery. The preliminary composite PMI fell to a six-month low in July of 47.7.

Spot: JPY109.85 (JPY111.10)

Median Bloomberg One-month Forecast JPY109.85 (JPY110.70)

One-month forward JPY109.80 (JPY111.05) One-month implied vol 5.4% (5.4%)

British Pound: Sterling reversed lower after recording a three-year high on June 1 near $1.4250 and did not look back. It dipped briefly below $1.38 for the first time since mid-April on the back of the hawkish Fed on June 16 to finish July at new highs for the month and above the downtrend line off the early June highs. A convincing move back above $1.40 would confirm a low is in place and a resumption of the bull move, for which we target $1.4350-$1.4375 in Q4. The postponement of the economy-wide re-opening until the middle of July, and a central bank looking past the uptick in CPI above the 2% medium-term target, weighed on sentiment. The central bank will update its economic forecasts in August, and both growth and inflation projections likely will be raised. The furlough program ends in September, and it may take a few months for a clear picture of the labor market to emerge. Nevertheless, the market has begun pricing in a rate hike for H1 22.

Spot: $1.3905 ($1.3830)

Median Bloomberg One-month Forecast $1.3930 ($1.3930)

One-month forward $1.3910 ($1.3835) One-month implied vol 6.6% (6.5%)

Canadian Dollar: The Canadian dollar reached its best level in six years in early June (~$0.8333 or CAD1.20) but has trended lower amid profit-taking and the broad gains in the US dollar. The usual drivers of the exchange rate: risk appetites, commodities, and rate differentials were not helpful guides recently. Canada has become among the most vaccinated countries, and the central bank was sufficiently confident in the economic outlook to continue to slow its bond purchases at the July meeting despite losing full-time positions each month in Q2. Speculators in the futures market have slashed the net long position from nearly 50k contracts (each CAD100k) to less than 13k contracts in late July. The downside correction in the Canadian dollar appears to have largely run its course, and we anticipate a better August after the heavier performance in July. Our initial target is around CAD1.2250-CAD1.2300.

Spot: CAD1.2475 (CAD 1.2400)

Median Bloomberg One-month Forecast CAD1.2435 (CAD1.2325)

One-month forward CAD1.2480 (CAD1.2405) One-month implied vol 6.8% (6.5%)

Australian Dollar: Since peaking in late February slightly above $0.8000, the Australian dollar has trended lower and by in late July briefly dipped below $0.7300, posting a nearly 9% loss over the past five months. The 50-day moving average ~$0.7570) fell below the 200-day moving average (~$0.7600) for the first time since June 2020, illustrating the downtrend after the strong recovery from the low near $0.5500 when the pandemic first stuck. The combination of a low vaccination rate and the highly contagious Delta variant forced new extended lockdowns for Sydney and social restrictions that have sapped the economy’s strength. It will likely slow the central bank’s exit from the extraordinary emergency measures. Indeed, the Reserve Bank of Australia is likely to boost its weekly bond-buying from A$5 bln to at least A$6 bln. A convincing break of $0.7300 could open the door for a return toward $0.7000, but we suspect the five-month downtrend is over and anticipate a recovery toward $0.7550 over the next several weeks.

Spot: $0.7345 ($0.7495)

Median Bloomberg One-Month Forecast $0.7425 ($0.7610)

One-month forward $0.7350 ($0.7500) One-month implied vol 8.9 (8.5%)

Mexican Peso: The dollar chopped higher against the peso in July and reached a high near MXN20.25 on July 21. It trended lower and, in late July, fell below the seven-week trendline support near MXN19.90. After finishing June less than 0.1% weaker, the greenback lost about 0.4% against the peso in July, which was the fifth consecutive month without a gain. The other notable LATAM currencies were the weakest three emerging market currencies (Chilean peso ~-4.1%, Colombian peso ~-4%, and the Brazilian real ~-3.8%). If the upper end of the dollar’s range has held, a break of MXN19.80 may warn a test on the lower end of the range (~MXN19.50-MXN19.60). The 5.75% year-over-year CPI for the first half of July and the highest core inflation for early July in more than 20-years keep expectations for another rate hike intact when Banxico meets on August 12. The market has another hike priced in for the September 30 meeting as well. The dispute with the US over measuring domestic content for auto production under USMCA could undermine Mexico’s role in the continental division of labor, but instead, producers in Mexico may choose to pay the WTO auto tariff standard of 2.5%. The IMF’s latest economic forecasts revised the projection for Mexican growth this year to 6.3% from the April projection of 5%.

Spot: MXN19.87 (MXN19.95)

Median Bloomberg One-Month Forecast MXN19.94 (MXN19.97)

One-month forward MXN19.95 (MXN20.02) One-month implied vol 10.5% (10.7%)

Chinese Yuan: The dollar spent most of July within the trading range that had emerged in late June found roughly between CNY6.45 and CNY6.4950. The range was maintained even after the PBOC unexpectedly cut reserve requirements by 50 bp (announced July 9). However, Beijing’s more aggressive enforcement of antitrust, discouragement IPOs abroad, making private education non-for-profit without foreign investment triggered sales of Chinese shares. It helped lift the dollar in late July to around CNY6.5150, its highest level in three months and just shy of the 200-day moving average. The pursuit of domestic policy objectives appears to be putting at risk strategic goals. A drying up of capital inflows from spooked foreign investors may have slow efforts to liberalize capital outflows that could eventually lead to making the yuan convertible. At the same time, China’s actions give a timely example of what holds the yuan back from a significant role in the world economy and why a technology solution (e.g., digital yuan) will not suffice. As the dollar briefly traded above the upper end of its recent range in July, the risk is that it slips through the lower-end range, which could spur a move toward CNY6.40.

Spot: CNY6.4615 (CNY6.4570)

Median Bloomberg One-month Forecast CNY6.4555 (CNY6.4360)

One-month forward CNY6.4780 (CNY6.4815) One-month implied vol 4.0% (4.7%)

Author:

- Marc Chandler, Chief Market Strategist, BBGFX

Compliments of Bannockburn Global Forex – a member of the EACCNY.