View Report as a PDF Here

Our Spotlight report reviews past and current performance of newer office buildings in the U.S.

The COVID-19 pandemic significantly disrupted the world, but perhaps no topic has gotten as much attention in real estate as that of the office sector. The future of work, the workplace and implications for office real estate remain as complex and uncertain as they were last year. What is certain, however, is that the physical office will continue to have some role to play in the future of work. And although there are a myriad of occupiers with vastly different needs, we know that newer, better quality office product, which usually outperforms, did so to a greater degree during the pandemic. And that trend is expected to stick.

Past Performance of Higher Quality Office Assets

Not all office product is created equal, and it is usually the case that Class A office outperforms the rest of the market. This has been true during both expansions and recessions, as well as within CBD and suburban geographies.

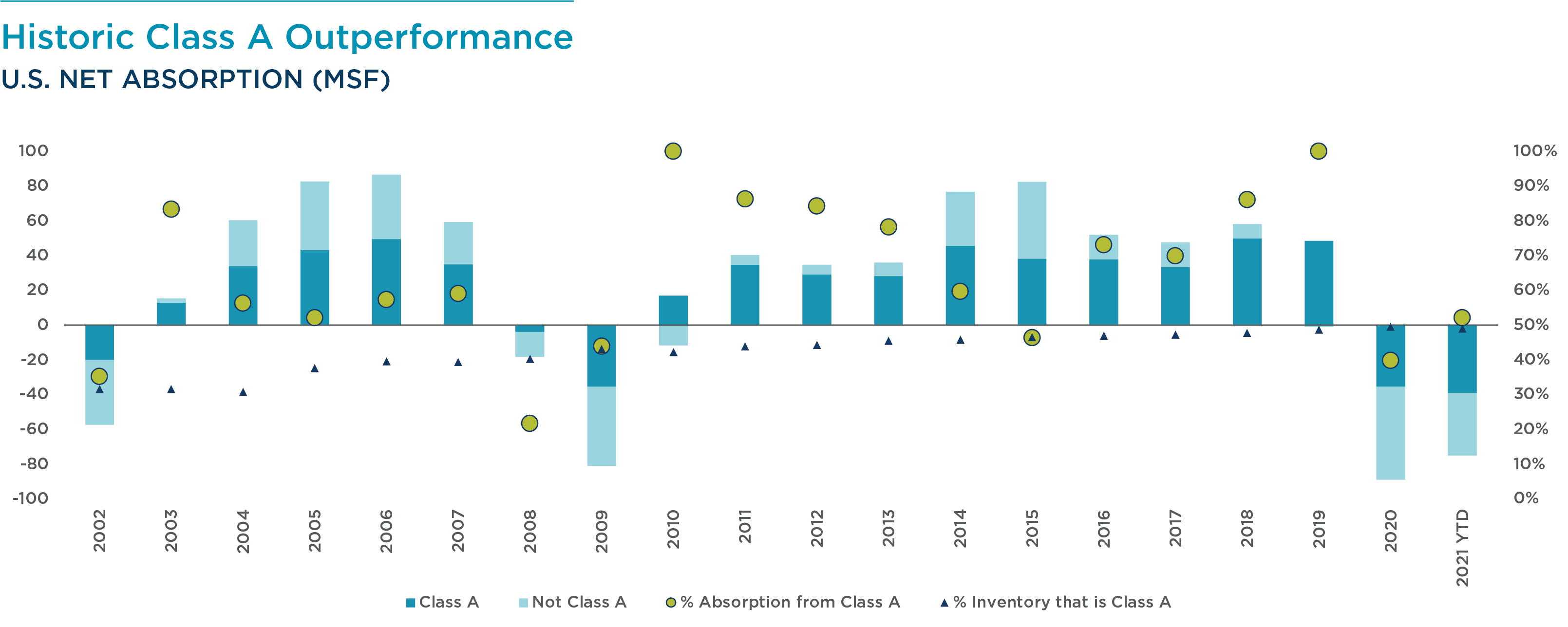

During prior expansions, Class A office garnered a disproportionate amount of absorption relative to its share of U.S. office stock. In fact, Class A office product has absorbed space during growth cycles at a rate that is 1.7 times its share of inventory; this ratio is 1.6 in CBDs and 1.8 in suburbs. During the expansion after the Dot Com recession, Class A office accounted for 61.6% of all absorption, versus accounting for 35.7% of the inventory. After the Great Financial Crisis (GFC), these shares were 78.4% and 45.0% respectively.

By contrast, Class A office tends to account for a lower share of net absorption when demand is negative. In other words, it outperforms during recessions. During the Dot Com, GFC and COVID-19 recessions, Class A office averaged 38.5% of negative absorption versus 42.7% of the stock. In some years, overall absorption was negative while Class A was positive, as was the case in 2003 in CBDs and in 2008 in the suburbs.

Since net absorption accounts for move-outs, these figures demonstrate clear demand outperformance. This is made possible by a historic average of 55.5% of all new leasing activity occurring in Class A assets, a 13-percentage point spread above the historic share of overall office inventory that is Class A (42.5%).

Past Performance of Newer Office Assets

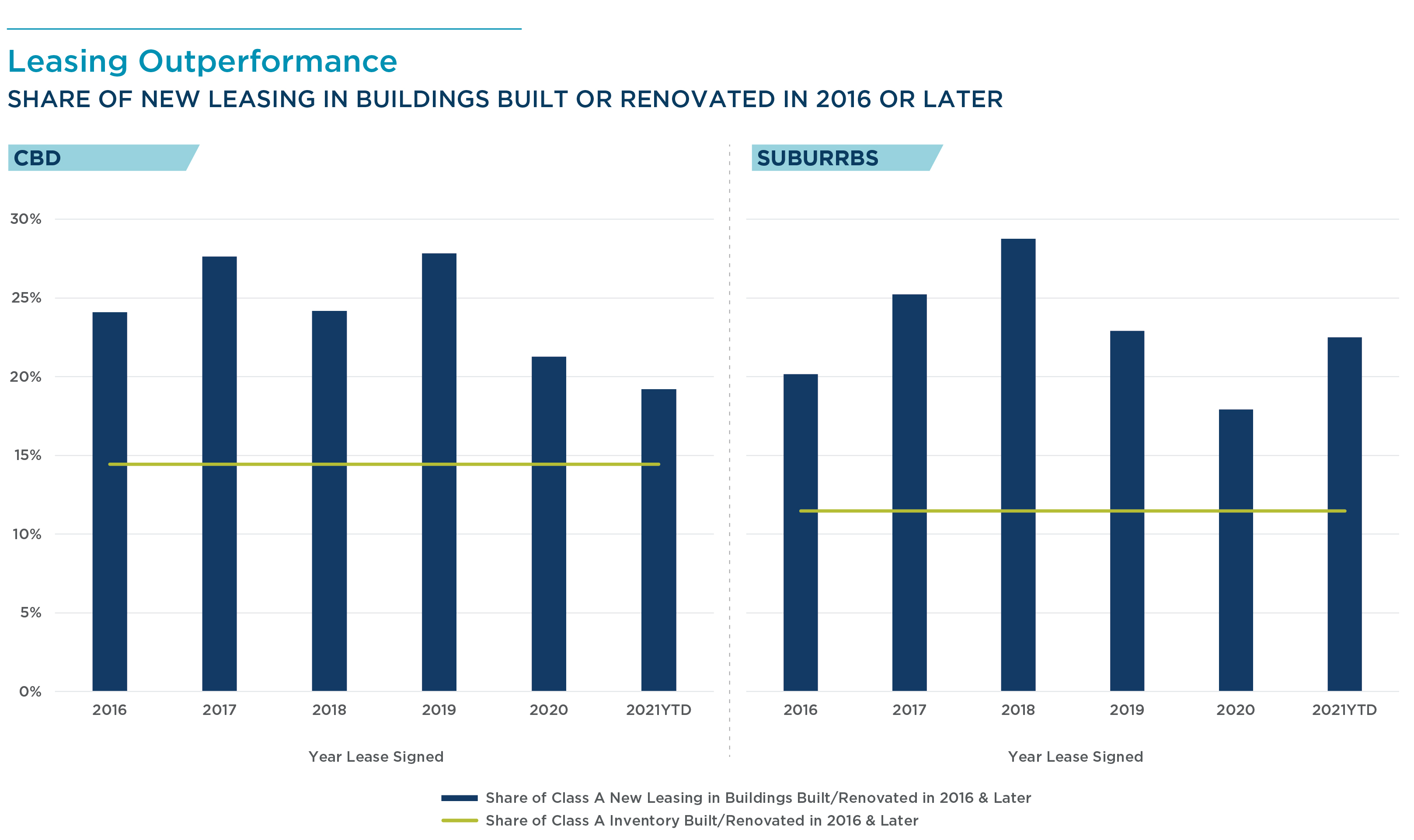

Within the Class A segment, newer assets also outperform. When looking at a sample of 2.5 billion square feet (sf) of Class A office stock, 12.6% was either newly constructed or underwent a substantial renovation within the last five years (a 2016 or later delivery date). However, the share of leasing activity that these buildings commanded in the past five years—including preleasing prior to delivery—was well above this share at 24.2%. In CBDs, despite new product accounting for 14.4% of Class A stock, 25.3% of new lease square footage in Class A buildings was signed in these assets. In the suburbs, these figures are 11.5% and 23.5%, respectively.

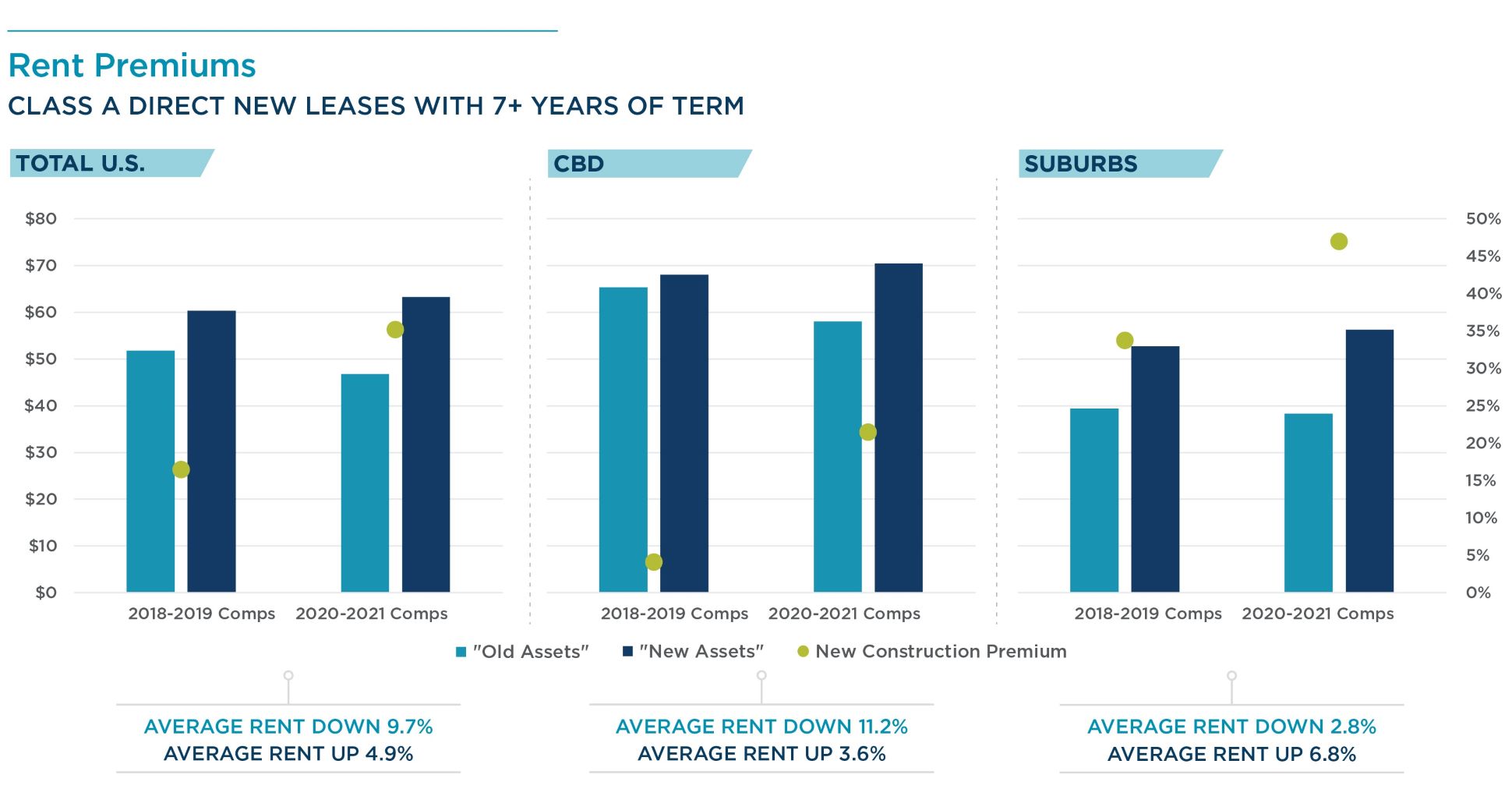

Comps from the 2018-2019 (pre-COVID-19) period reveal that the premium paid in achieved rents in these new assets was 16.4% nationwide (compared to achieved rents in buildings that delivered in 2015 or earlier, but that are also Class A). This analysis includes new, direct leases with at least seven years of term and is inclusive of pre-leasing on deliveries that had yet to hit the market before the pandemic. The premium was wider in suburban markets, at 33.1%, versus in CBDs (4.1%).

Pandemic Performance of Higher Quality and Newer Office Assets

Since the pandemic began, fundamentals have deteriorated. However, many of the same demand trends that existed pre-COVID-19 remain true. From an absorption perspective in 2020, Class A was hit less hard, accounting for about 40% of negative absorption but about 50% of total U.S. office stock. In 2021, Class A has accounted for about 50% of negative absorption, which is right in line with its share of office stock. Historically this “proportionate” impact has happened in each recession (in 2002 and in 2009) just prior to a pick-up in absorption that is driven by Class A demand specifically.

Given the unique aspects of COVID-19, while the timing of a pick-up in absorption is less certain than usual, it is clear that Class A will outpace the overall market as it has in early stages of prior expansions. New leases signed during the pandemic have been concentrated in Class A offices: 56% of new leases signed in 2020 and 2021 were in Class A assets, exactly on par with the pre-COVID-19 trend. As Figure 2 shows, new leases signed are also concentrated in newer Class A offices at rates that are on par with pre-COVID-19 trends.

While demand trends have remained in line with pre-pandemic patterns, there has been a shift in the premium paid for newer assets within the Class A universe. When looking at comparable comps signed in 2020 through mid-year 2021, the premium for newer assets is 35.2%, more than twice its immediate pre-COVID-19 level. Part of the widening is due to a decline in achieved rent levels on older Class A assets, while another part of it is due to a higher level of achieved rents in new assets. In suburban markets, achieved rents in older assets declined only slightly (down 2.8%) whereas achieved rents in newer assets are up 6.8%. In CBDs, achieved rents on new assets are also up, but to a lesser degree (3.6%) whereas achieved rents on older assets are down 11.2%.

While these trends are perhaps reflective of the relatively more conservative pipeline in suburban office markets in the last cycle and a slightly higher degree of resilience in absorption throughout the pandemic in suburban markets, it is also due to a higher degree of elasticity in CBD rents. Rents in CBDs have tended to move more sharply than those in suburbs after controlling for market and economic factors. These findings are consistent with anecdotes of a flight to quality and intense competition among occupiers for the very best space. They are also consistent with the reality that older and lower quality office stock will bear the brunt of current market conditions.

Not Just Fundamentals, New Office Outperforming in Capital Markets

Newer product outperformance extends into the capital markets as well. In 2007, the proportion of class A office sales where the building had been delivered or renovated within the preceding five years reached a record low of 19.1%. As the GFC unfolded, this share rose to 38.2% by 2010. As the market recovered, the newer construction share pulled back but remained around 32% of class A office sales. However, since 2016, the share has been growing as part of a broader shift in investor appetite towards the highest quality office product. The pandemic has further accelerated this shift—the newer construction share rose to 42.7% in 2020 and is at 49.8% in 2021 through the second quarter. These patterns encompass both CBD and suburban office markets, major and secondary markets.

The performance gap between newer and older class A product is also reflected in pricing. From 2010 to 2019, newer Class A office cap rates averaged 12 basis points (bps) less than those of older class A product. Since the pandemic began, the newer construction premium has increased to 43 bps on average. This trend has been particularly salient in suburban office markets, and while it has been a persistent feature of secondary markets, it has emerged in major markets since the beginning of the pandemic.

Looking Ahead

In the post-COVID-19 era, the quality of office space will become more important than ever. With a more hybrid workforce, companies will increasingly rely on attributes of the office to reinforce other motivations (such as bonding, collaborating, learning and development) for coming into the workplace. Differentiation with amenities and quality have played into the historic trend of outperformance of Class A and specifically newer Class A office assets. This outperformance has remained, and in some cases, widened during the pandemic. Two-thirds of employees External Link want more in-person work or collaboration post-pandemic and employee engagement is currently 4-8 percentage points higher among employees frequenting the office during the pandemic. Companies that offer high-quality, well-located, amenities office spaces that excite workers and encourage in-office attendance will have a competitive advantage.

Author:

- Rebecca Rockey, Head of Economic Analysis & Forecasting, Global Research

Compliments of Cushman & Wakefield – a member of the EACCNY.