Under the bill, businesses would be given more time to use the loans and greater flexibility to make needed expenditures and still qualify for forgiveness.

The bill was approved, 417-1, and now goes to the Senate.

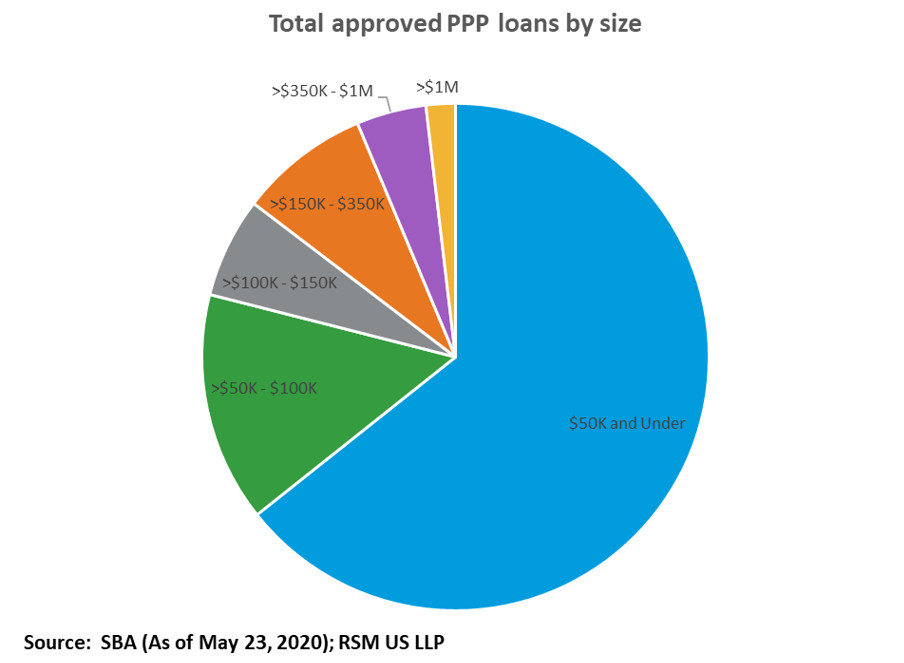

Where the program stands

Almost 4.5 million loans totaling $511 billion had been made under the Paycheck Protection Program as of May 23. The average loan size is $116,000, with more than 64% of the loans for $50,000 or less.

The $349 billion Paycheck Protection Program was signed into law on March 27 as part of the $2.39 trillion CARES Act and is administered by the Small Business Administration through its 7(a) lending program in which the SBA guarantees loans made by banks to qualifying borrowers.

The program, though, had a rocky launch, hampered by technical issues and glitches, as it sought to help small businesses retain employees through the economic fallout from the coronavirus. The first round of funding ran out in two weeks. A second round of funding increased the program to $649 billion.

The program now has less than $150 billion to lend out to qualified businesses.

The highlights

Here are key provisions of the bill, H.R. 7010:

• Extend the PPP loan forgiveness period to include costs incurred over 24 weeks after a loan is issued or December 31, 2020, whichever comes first. Current borrowers could elect to continue using the current eight-week period after this bill is enacted.

• Extend the deadline to apply for a PPP loan from June 30 to December 31, 2020.

• Require at least 60% of forgiven loan amounts to come from payroll expenses.

• Removed the six-month deferral period by allowing borrowers to defer principal and interest payment on PPP loans until the SBA compensates lenders for any forgiven amounts. Borrowers that don’t apply for forgiveness would be given at least 10 months after the program expires to start making payments.

• Extend the period in which loans can be forgiven from June 30 to December 31, 2020, if businesses restore staffing or salary levels that were previously reduced. This provision would apply from February 15, 2020, through 30 days after enactment of the CARES Act, which was signed into law on March 27.

• Maintain forgiveness amounts for businesses that document their inability to rehire workers employed as of February 15, 2020, and their inability to find similar qualified workers by the end of the year.

• Provide that the amount of loan forgiveness will not be reduced if a business could show that it couldn’t resume businesses levels before February 15, 2020, because it was following federal requirements for sanitization or social distancing.

• Allow employers to defer the 6.2% employer portion of Social Security payroll taxes if they had a PPP loan forgiven.

• Extend the minimum maturity period of PPP loans from two to five years. This provision would apply to PPP loans issued after the measure is enacted, but open the possibility for borrowers and lenders to mutually agree to modify current loans.

• Most of the changes, except for the last one, would apply retroactively to the enactment of the CARES Act.

The takeaway

This bill is a huge step in the right direction to make the needed changes within the original CARES Act. Small and medium-sized businesses owners will have a better chance of having their PPP loans forgiven if the relaxed rules within this bill are signed into law.

AUTHOR:

• Jason Kuruvilla

Compliments of RSM US LLP – a member of the EACCNY.