The Regulation on Interchange Fees for Card-based payment transactions entered into force in June 2015. It is aimed at addressing the widely varying and excessive hidden interchange fees which are an obstacle to the Single Market and a barrier to innovation.

The Regulation caps the interchange fees for the most widely-used cards and imposes transparency obligations on banks and retailers to improve the functioning of the payment market for all cards. The rules on interchange fee caps have applied since December 2015, while the rules on transparency apply from 9 June 2016.

What are interchange fees?

Each time a consumer uses a credit, debit or prepaid card to buy something in a shop or online, the retailer’s bank (the “acquiring bank”) pays a fee called “interchange fee” to the consumer’s bank that issued the card (the “issuing bank”). As retailers generally incorporate interchange fees in the prices they charge consumers, these fees increase the retail prices of goods and services.

Interchange fees are normally set by operators of payment card schemes, such as Visa or MasterCard, or the banking community. Retailers have no possibility to influence the level of the fees, as they are not involved in the process.

Different types of cards are usually subject to different levels of interchange fees. For example, credit cards usually carry higher interchange fees than debit cards. These cards are thus more expensive for retailers to accept. Before the entry into force of the Regulation on interchange fees, interchange fee levels also used to vary a lot between Member States.

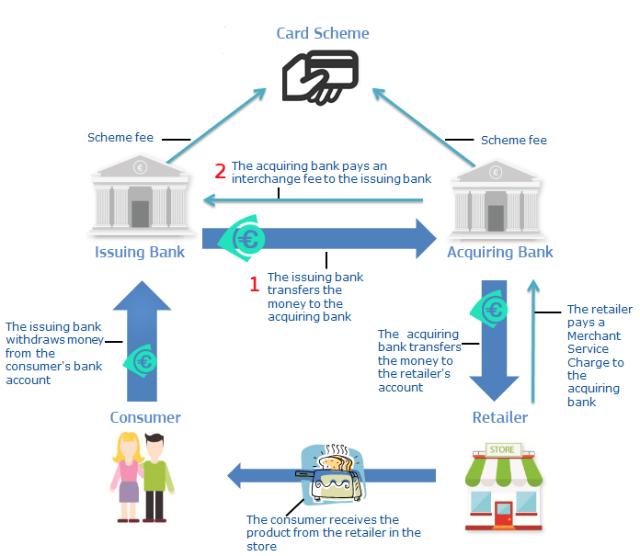

When a consumer pays a retailer by card, several other actors are involved in the payment transaction. Most schemes operate as a so-called ‘four party’ card scheme:

Arrow 1 show how the purchase price is transferred from the consumer’s to the retailer’s bank account. Arrow 2 shows the interchange fee paid from the acquiring bank to the issuing bank. Most four-party schemes require the acquirer to pay an interchange fee to the issuer every time a transaction is made.

What was the problem with interchange fees?

Usually, competition leads to lower prices since companies compete by offering lower prices than their competitors. In the case of interchange fees, the opposite occurs. Since issuing banks benefit from interchange fee revenues, card schemes compete for the issuing banks by offering higherinterchange fees. These fees are a cost for retailers which increase the price of their products.Interchange fees are therefore, indirectly, paid by consumers. Consumers and retailers are often unaware of the level of these fees. In addition, cardholders are encouraged through rewards offered by their bank to use cards that generate higher fees for the bank. This has consequences for both retailers and consumers:

If a retailer refuses commonly-used cards, there is a risk that consumers would choose to go to its competitors. Individual retailers tend thus to accept high costs for card payments to keep and grow their sales.

Retailers recover higher costs due to ever increasing interchange fees by increasing retail prices. As a result, the prices increase for all consumers, including those who pay cash or use cheaper payment cards, because the higher fees of more expensive cards are spread out and passed on to all.

The Regulation on interchange fees for card-based payment transactions aims at changing this situation to the benefit of retailers and consumers.

What are they key benefits of the Interchange Fees Regulation?

The Interchange Fees Regulation will bring significant benefits for consumers and retailers, notably by reducing the costs of card payments. First of all, the capping of interchange fees should result in lower fees charged by banks to retailers for processing card payments. All retailers should in time benefit from this: thanks to improved transparency about the level of interchange fees, retailers are in a better position to ensure that their costs reflect interchange fees charged. These cost savings would then be passed on to consumers through lower prices for goods and services.

In addition, more retailers are likely to accept card payments as they would overall pay less for such transactions. This would allow consumers to shop using cards more widely than today.

Last but not least, the Regulation paves the way for innovative payment technologies to be rolled out. High interchange fees have been an important source of revenue for issuing banks, representing about €13 billion a year in the EU and so banks have had an incentive to stick to the existing system. Given the key role that banks play in payments, the fact that banks expected varying levels of interchange fee throughout the EU made it very difficult for new entrants and new innovative payment services to enter the market. The caps on the interchange fees should remove or limit these incentives and make it easier for new players and services to enter the market.

What are they key provisions of the Interchange Fees Regulation?

1) Capping unreasonably high interchange fees (applicable since December 2015)

Interchange fees are indirectly paid by retailers, who subsequently pass the fee on to all consumers in the form of higher prices. Reducing unreasonably high interchange fees, should lower the costs to retailers for processing card payments, who would then be under pressure to pass on the savings to consumers through lower prices for goods and services.

The Regulation ensures that interchange fees are capped at a level such that retailers’ average costs are not higher for card than for cash payments. Therefore, the Regulation caps interchange fees for consumer debit cards to 0.2 % and consumer credit cards to 0.3 % of the value of the transaction.

The reduction of the interchange fees also makes it possible to abandon surcharging on consumer card payments (which is technically achieved in 2018 through the Payment Services Directive II).

2) Consumers and retailers can choose most efficient payment type (applicable since June 2016)

‘Co-badging’ means that a single device, e.g. a card, a smartphone or other devices may contain different payment means or brands (e.g. Visa, MasterCard, Maestro or AMEX). Consumers can now select and retailers can promote the most cost-efficient brand when paying with co-badged cards to minimise costs. In particular:

- Retailers can install priority selection

Retailers have the option of installing a default choice of application in their payment terminals, based on the most cost-efficient brand for them and – as a consequence – for their customers.

- Consumers have the last say

Consumers have the right to ‘override’ such an automatic priority selection with their own brand of preference within the brands and applications accepted by the retailer – when this is technically feasible.

- Consumers will be informed.

Retailers will have to inform consumers clearly which cards they accept and which is their preferred payment means. Where technically possible, they should also inform consumers how they can override the merchant’s preferred choice and make the final selection of payment means.

Previously, the preferred brand was typically selected by card issuing banks or card operating schemes, which have an interest in selecting the brand generating the highest interchange fee for them.

3) Co-badging – one card for all brands (applicable since June 2016)

The ability to choose the preferred payment type will become even more important going forward, since the Regulation gives consumers the right to require their bank to co-badge their device with all other brands offered as compatible apps (for a wallet) or other card products offered by the bank (for a card).

The bank can, however, refuse to offer the customer a given card product (e.g. a premium card).

4) More transparency on card transaction fees

Previously, interchange fees were hidden not only from the public eye but also unknown to retailers. They were not able to compare the fees they paid to banks for processing the transaction (the “Merchant Service Charge”) with the interchange fee paid by the bank. This lack of transparency likely resulted in higher merchant service charges that were ultimately passed on to consumers. The Regulation will address this including as follows:

No single “blended” fee (applicable since December 2015)

In addition, upon execution of eachindividual card-based payment transaction, retailers should receive, unless they decide otherwise, information describing the amount of the paymentinterested by the transaction andthe amount of any charge linked to the transactions, indicating separately the interchange fees paid by the bank and the Merchant Service Charge.

Clarity on charges in contracts (applicable since June 2016)

In their contracts with retailers, acquiring banks will have to specify individually the different fees they will charge (merchant service charges, interchange fees, scheme fees) for each category and brand of payment cards.

5) Introducing more competition in the payments market

No territorial restrictions in licences (applicable since December 2015)

To promote competition across the Single Market, companies who are licensed to issue cards or acquire card transactions should be able to extend their activities to the whole of the European Union. This is why the Regulation bans territorial restrictions in licences.

Separation of payment schemes and processing entities (applicable since June 2016)

Processing refers to the communication and IT process needed to make a card payment. Card schemes often have their own subsidiary for the processing of payment transactions but there are many other independent companies that provide processing services. The Regulation requires independence between card schemes and their processing entities. It prevents card schemes from favouring their subsidiaries over competing processing entities and from bundling the services of their processing entity with other services that the card schemes offers. The purpose of this part of the Regulation is to make the processing market more competitive and to enable banks and retailers to choose the best processor for their card transactions.

How will the Commission measure the impact of the Regulation?

The Commission is currently in the process of gathering information to establish the state of the market in 2015, before the entry into force of the Regulation, by collecting information from banks and schemes directly from these market players. The Commission will compare the information gathered now to the state of the market in 2018 and publish a report on the results in 2019.

Compliments of the European Commission