The third quarter of 2016 featured the reversal of several trends seen earlier in the year, most notably in pre-money valuations, which increased substantially for all rounds. The gain in pre-money valuations also drove a decline in the percentage of down rounds for the quarter, which fell to 9%, the lowest share in more than a year and far below the five-year median (from Q4 2011 through Q3 2016) of 16%. If these strong valuations continue through the fourth quarter, 2016 cumulative pre-money valuations may catch up to those of 2015. In addition, median dollar amounts raised are on track to exceed those of 2015 for all but Series C and later rounds.

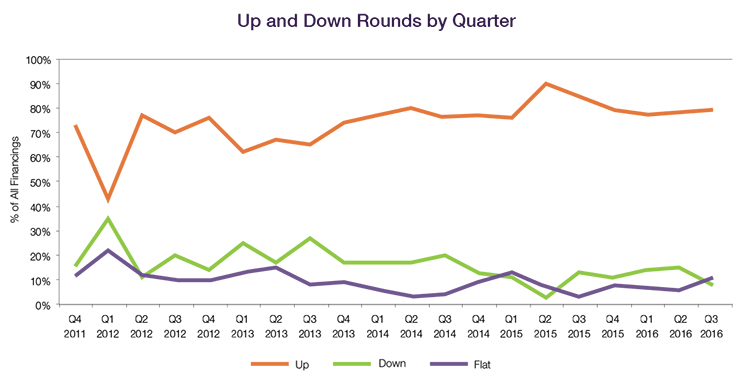

Up and Down Rounds

Down rounds fell to their lowest percentage of overall deals in several quarters, representing 9% of post-Series A financings in Q3 2016, as compared to 16% in Q2, while flat rounds increased from 7% in Q2 to 12% in Q3. Seventy-nine percent of all financings were up rounds in Q3 2016, only slightly more than in Q2, and four percentage points above their five-year median of 75%.

|

|

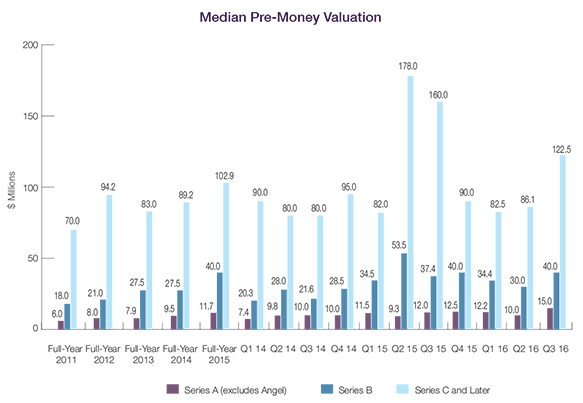

Valuations

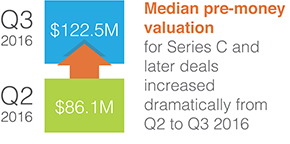

Pre-money valuations rose to nearly match the five-year highs of Q2 2015, with the median valuation for Series A and Seed financings exceeding that of all prior quarters tracked, at $15.0 million—well above the five-year median of $8.0 million. The median pre-money valuation for Series B rounds remained strong at $40.0 million—less than the historic high median of $53.5 million seen in Q2 2015, but more than the five-year median of $30.0 million. The median pre-money valuation for Series C and later deals spiked to $122.5 million from $86.1 million in Q2 2016, a number exceeded only twice in the last five years ($178.0 million in Q2 2015 and $160.0 million in Q3 2015).

Amounts Raised

Amounts Raised

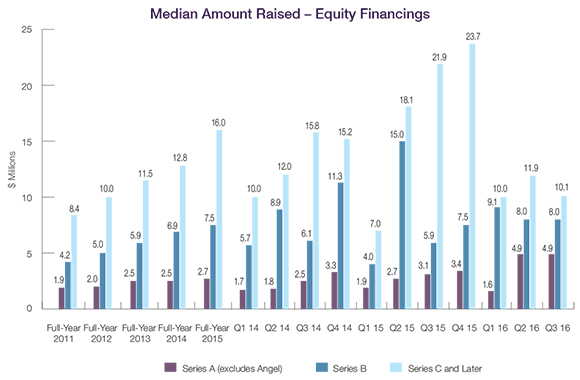

The $4.9 million median amount raised in Series A and Seed transactions in Q3 2016 duplicated the median amount in Q2, with the two quarters representing the highest medians of the past five years. The median amount raised in Series B financings in Q3 2016 also duplicated the median amount raised in Q2, at $8.0 million. In contrast, the median amount raised in Series C and later transactions fell from $11.9 million in Q2 2016 to $10.1 million in Q3, nearly matching the Q1 median and well below the 2015 median of $16.0 million. The somewhat lower median amounts raised for Series C and later transactions so far this year may reflect strategic decisions by private companies to avoid raising relatively large amounts of money at late-stage valuations that are meaningfully below the peaks reached in late 2015.

Deal Terms – Preferred

The use of senior liquidation preferences rose in Series B and later rounds, increasing modestly from 33% of all such rounds in 2015 to 41% in Q1-Q3 2016. Down rounds show the most dramatic increase, with senior liquidation preferences jumping from 35% of such rounds in 2015 to 53% of such rounds in Q1-Q3 2016. Meanwhile, pari passu liquidation preferences in down rounds dropped from 53% in 2015 to 33% in Q1-Q3 2016.

The percentage of financings having a liquidation preference with participation remained constant for all financings. The proportion of down rounds with participating liquidation preferences, however, remained at a low of 20% for Q1-Q3 2016. This may be a statistical anomaly resulting from the small number of down rounds so far this year, or it may reflect decisions to forgo such rights in transactions where prior rounds also lacked such rights.

Investors received broad-based, anti-dilution protection in 93% of all deals so far in 2016.

Data on deal terms such as liquidation preferences, dividends, and others are set forth in the table below. To see how the terms tracked in the table can be used in the context of a financing, we encourage you to draft a term sheet using our automated Term Sheet Generator, which is available in the Start-Ups and Venture Capital section of the firm’s website at www.wsgr.com.

Private Company Financing Trends (WSGR Deals)1

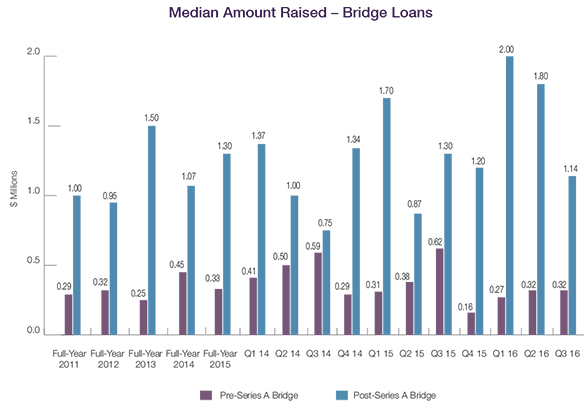

Bridge Loans

The median amount raised for pre-Series A loans was $0.32 million in Q3 2016, the same as in Q2, while the median amount raised for post-Series A loans dropped from $2.0 million in Q1 2016 and $1.8 million in Q2 to $1.1 million in Q3.

Deal Terms – Bridge Loans

Only 4% of pre-Series A loans have had interest rates greater than 8% so far in 2016. For post-Series A loans, rates above 8% climbed from 13% of deals in 2015 to 18% of deals in Q1-Q3 2016, while 54% of such loans bore rates of less than 8%, consistent with what was seen in 2015.

Price caps and discounts upon conversion became more popular for pre-Series A bridge loans. Price caps increased from 64% of deals in 2015 to 83% of deals in Q1-Q3 2016, and discounts on conversion of pre-Series A loans also rose slightly, from 78% of deals in 2015 to 83% of deals in Q1-Q3 2016. On the other hand, the size of discounts dropped, with the percentage featuring a discount of over 20% declining from 16% of such loans in 2015 to 11% so far in 2016. Post-Series A bridge loans show little change for these terms compared to 2015.

Compliments of Wilson Sonsini Goodrich & Rosati – a member of the EACCNY