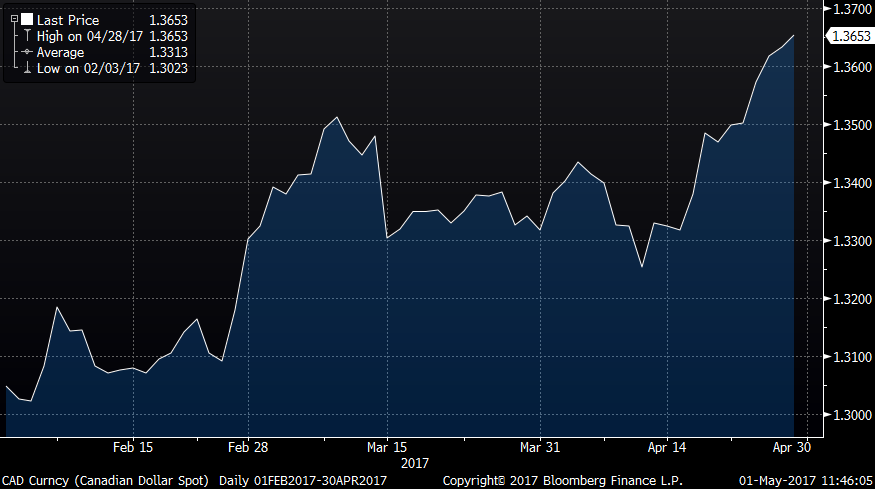

USD/CAD

After early month gains on a stronger oil price and some stronger Canadian data, the CAD fell back in the second half of April as the oil price weakened and the US imposed a tariff on Canadian lumber. Technically, USD/CAD had found the expected strong support near 1.32 early in the month, and once the news turned against the CAD gains were quite swift. At this stage, the lumber tariff looks unlikely to be extended to other goods, so is far less serious that a general border adjustment tax, but this remains a possible way for Congress to propose shoring up the US budget against the proposed tax cuts, and the lumber tax should highlight the vulnerability of Canada should the US take this course. As with most other USD pairs, USD/CAD will be sensitive to fluctuations in expectations about Fed policy coming into the June Fed meeting, but the downside now seems well protected at 1.32 and upside to the 1.38-1.40 area is targeted.

Three-Month USD/CAD:

|