The Iran Conflict, Tariff Uncertainty, and Geopolitics Continue to Impact Supply Chains All Over – When Will It End?

Global Ports

The Headlines: The ongoing conflict with Iran and its impact on shipping through the Strait of Hormuz and the Red Sea are an obvious challenge for the region. And the disruptions have quickly spread globally, up and down supply chains, creating immediate delays at Asian ports (particularly China and India). Getting less attention is the tension over control of ports outside the Panama Canal, with China having threatened a “high price” if a Panamanian court ruling against it is upheld. Overall, global ocean volumes are strong in most regions (excluding the U.S).

What’s Important: Few would have thought global supply chains would get MORE complex at this point in 2026, but here we are. Ports and supply chains must now navigate an operating environment where uncertainty equals that of any point during peak tariff chaos and possibly COVID. For companies, flexibility and planning are more critical than ever, making it essential to leverage visibility tools and technology-driven partners to respond quickly to market shifts and maintain alignment across suppliers and carriers.

European Update

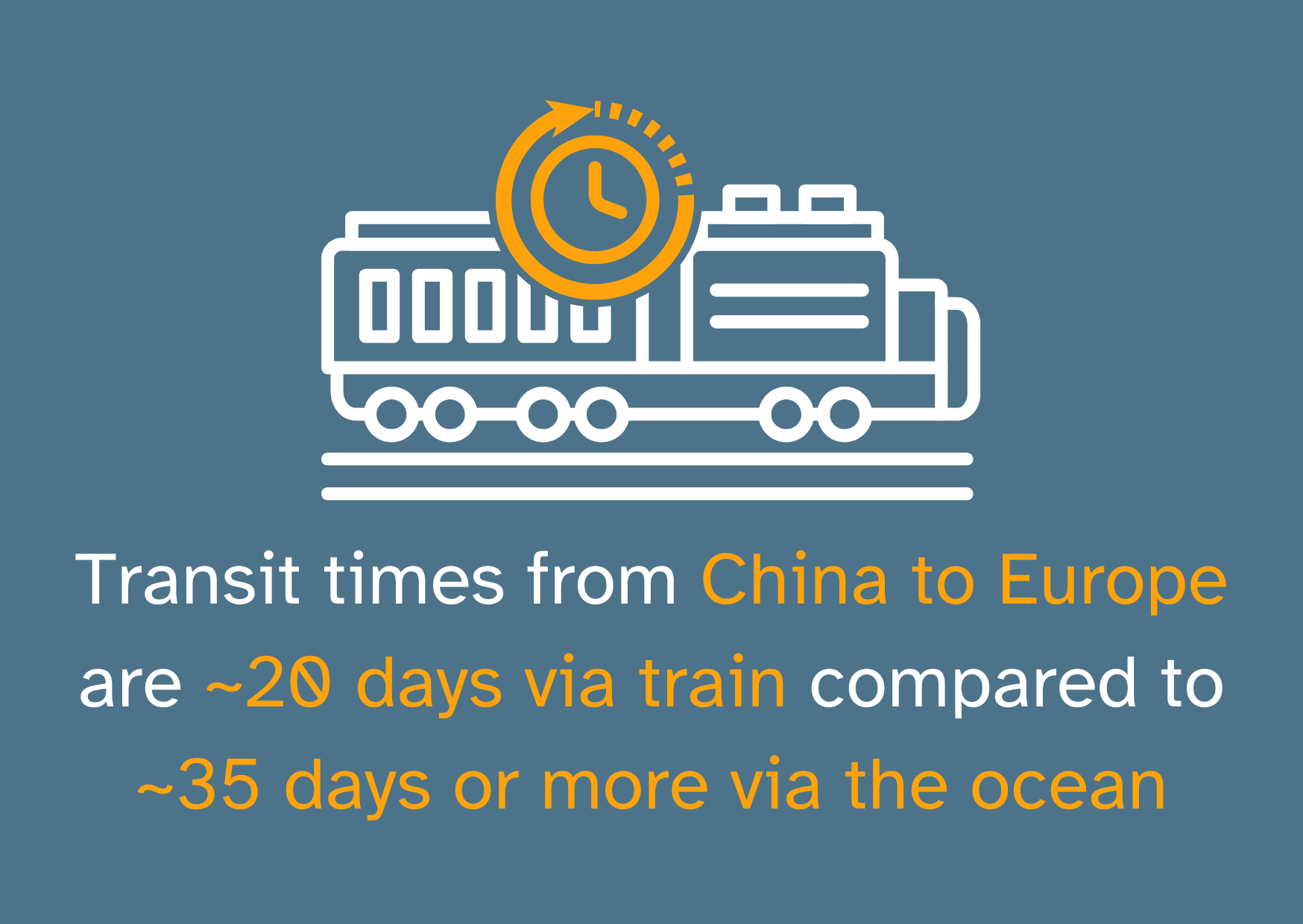

The Headlines: Europe’s supply chain landscape continues to be shaped more by geopolitical risk and structural shifts than by market demand. Years of persistent instability in the Black Sea region and ongoing disruptions in the Persian Gulf and Red Sea continue to create unwelcome supply chain chokepoints, which are keeping freight costs high and routes under pressure. A positive is that China–Europe rail service continues to improve, providing a competitive alternative with advantages in lead times and routing flexibility.

What’s Important: Volatile fuel prices, higher operating costs, and shifting carrier strategies mean that routing decisions carry more weight than in recent years. Mode choice is increasingly a matter of balancing cost, speed, and stability rather than simply choosing the least expensive option. Europe will remain one of the most operationally complex regions in 2026, and strategic planning that incorporates mode flexibility and risk‑aware routing is necessary for maintaining service levels and margins.

Ocean Freight

The Headlines: Ocean freight markets have unwillingly entered a period of heightened uncertainty, which would have seemed hard to believe was possible in the middle of February. Bunker costs and rates have been volatile since the start of the Iran conflict. And war-risk surcharges and higher insurance premiums are putting additional pressure on shippers. At the same time, U.S. import volumes are projected to further soften in 2026 amid slowing consumer demand, which will only add to rate volatility.

What’s Important: Like other parts of the global supply chain, the ocean freight market is being shaped as much by network risk and instability as by demand and volume. Expect short-term market shocks that impact rates and service to continue. Flexible routing, multi-carrier options, and contingency planning are essential to deal with sudden rate spikes or service interruptions. The takeaway: even in a down market, ocean freight requires strategic planning and flexible management.

Air Freight

The Headlines: Global air cargo continues to see elevated demand, though growth has moderated slightly in early 2026. Following record volumes in 2025, overall cargo tonnage remains high, supported by the recovery of passenger flights. However, demand is becoming more segmented by industry, with technology, healthcare, and time-sensitive industrial goods driving the strongest volumes. A driver of the past few years, e-commerce shipments show signs of early softening.

What’s Important: No surprise, but geopolitical disruptions and shifting trade lanes, particularly in Europe and the Middle East, have added complexity to routing and scheduling, influencing carrier operations and capacity planning. Without a clear strategy, shippers may face higher costs, limited space during peak periods, and reduced flexibility if they must make sudden route adjustments or shift capacity. To maintain service reliability, companies should focus on forecasting demand by product type, engaging with carriers early, and exploring multiple routing options.

N. America Inland Trends

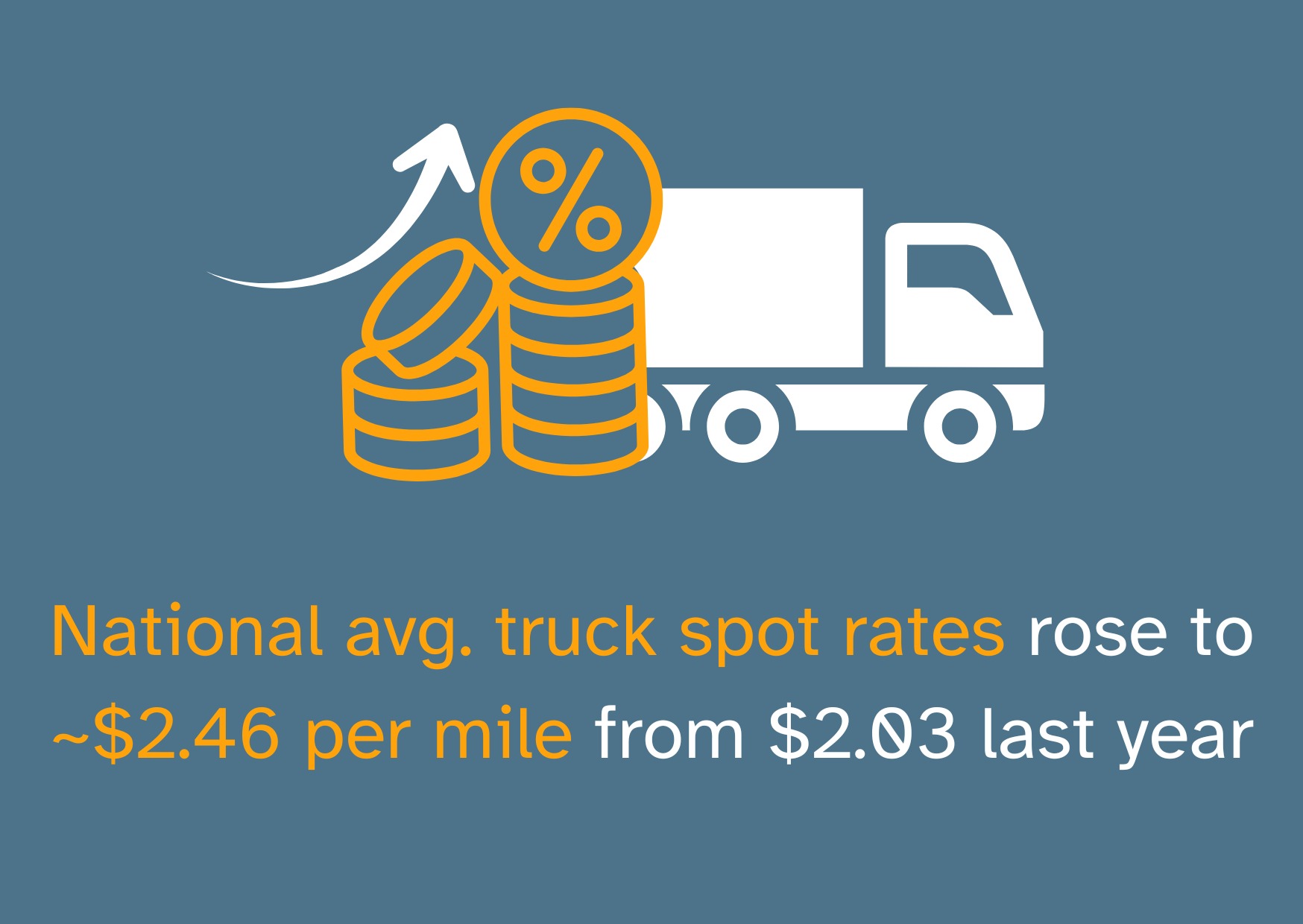

The Headlines: There is a growing demand for N. American TL carriers, as manufacturing activity expanded for a 2nd consecutive month in February (but only the 3rd time in 3+ years), according to the ISM’s latest survey. Along with it, however, is growing competition from carriers and 3PLs, which benefits shippers. At the same time, smaller carriers continue to exit the market due to financial pressures, which is shrinking overall capacity and reducing some competition.

What’s Important: The inland market continues to favor buyers, with trucking near cyclical lows and selective intermodal lanes offering cost advantages on longer hauls. But, signs are that this advantage is lessening. If the market continues to shift, Companies should focus on flexible routing, multi-modal integration, and early engagement with carriers to secure space and maintain dependable delivery schedules, especially for time-sensitive or high-value freight.

U.S. Logistics Manager’s Index

The Headlines: The most recent Logistics Manager’s Index (LMI) came in at 61.5, up from January’s 59.6, marking the fastest expansion rate since February 2025. Transportation metrics are showing particularly strong growth, while transportation capacity is contracting, signaling tighter conditions. In contrast, warehousing capacity shows little movement, and inventory levels are being managed more conservatively. Warehousing prices continue to rise, though at a slower pace than the previous year.

What’s Important: The LMI survey shows some contrasts: while warehousing pressures are easing slightly, transportation pressures are tightening, putting upward pressure on shipping rates. This evolving market speaks to the value and importance of visibility across the supply chains to enable more proactive coordination with logistics partners, suppliers, and customers. In the current market, companies that align PO and inventory management with transportation realities are best positioned to mitigate rising costs and preserve service reliability.

Supply Chain Risk

The Headlines: The 2nd Quarter 2026 LRMI Report shows that overall supply chain risk remains elevated, with continued concern across multiple categories and most risks staying above neutral. The report highlights economic, government intervention, and cybersecurity risks among the most significant, reflecting persistent macroeconomic uncertainty, regulatory challenges, and digital threats facing organizations. The findings suggest that some risks may be stabilizing, but note that many survey responses came in prior to the conflict in Iran.

What’s Important: The implication of the survey, no matter when the replies came in, is that importers should expect continued disruption and volatility. The conflict in Iran only makes that more pronounced. Much of the same advice from the past year holds true as importers can take on the challenges by diversifying sourcing options and building buffer inventory for critical goods to reduce dependency on any single risk point. Additionally, investing in better supply chain visibility tools and scenario planning will help importers anticipate disruptions earlier and respond more effectively.

IEEPA Tariffs & Trade Ruling

The Headlines: Here is an update on the two major trade and geopolitical events impacting supply chains right now: TARIFFS and the IRAN CONFLICT.

TARIFFS: Toward the end of February, the U.S. Supreme Court determined that IEEPA tariffs were unlawful, triggering a new series of developments. The ruling, however, did not provide the clarity importers were hoping for. Below is what we know right now:

- IEEPA tariffs ceased being collected shortly after the ruling took effect.

- Section 122 tariffs were promptly introduced at 10% as a substitute for IEEPA duties, although their legal standing was quickly challenged.

- Additional tariffs, such as Section 232 tariffs covering metals, automotive, and related categories, remain in effect.

- The CIT has directed that tariffs be refunded, though the CBP does not yet have a system in place to facilitate this. It is hoped that a refund process will be established within the coming weeks.

- Separately, new Section 301 investigations are now in progress, which could result in additional country-specific tariffs if unfair trade practices are substantiated.

IRAN CONFLICT: Supply chain disruptions stemming from the conflict emerged almost immediately, and there is little indication that conditions will improve in the near term.

- Fuel prices have climbed and continue to fluctuate, as have rates for ocean and air freight.

- Additional costs, including War Risk surcharges and elevated insurance premiums, are adding to overall shipping expenses.

- Ocean freight shipments are experiencing delays of up to two weeks as carriers reroute away from the affected region.

- Ongoing uncertainty is complicating supply chain planning across the board. Given how interconnected global supply chains are, disruptions in the Middle East have already rippled into Asian ports, generating further delays.

What’s Important: Uncertainty stemming from the conflict in Iran and ongoing tariff changes requires importers to be flexible in their supply chains and stay on top of new developments. Neither disruption appears to be going away anytime soon. And a reasonable person could expect a few new surprises coming later this year… whatever they might be. Supply chain management is difficult right now, and the companies that get through it will do so by emphasizing communication and leaning on trusted partnerships. The Jaguar Freight team is always available to answer questions and offer advice to anyone. We are eager to help.

Compliments of Jaguar Freight – a member of the EACCNY